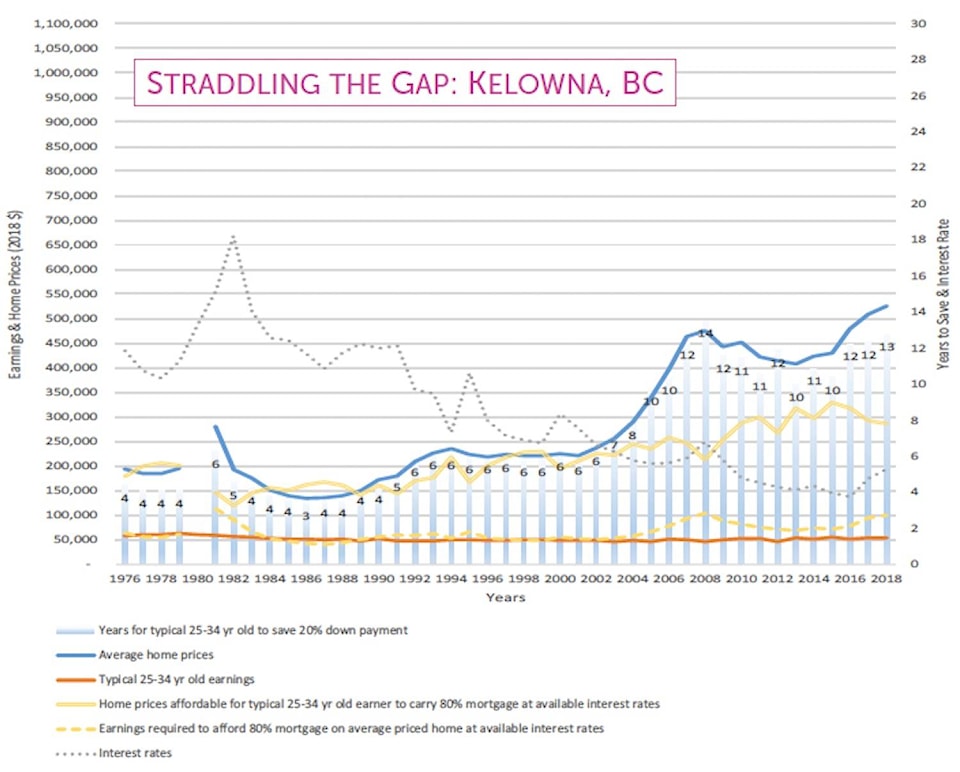

House prices in Kelowna would need to be cut nearly in half for mortgages to be affordable for young people, a new study finds.

According to a Generation Squeeze study entitled Straddling the Gap: A troubling portrait of home prices, earnings and affordability for younger Canadians, average home prices would need to fall $239,000—about half of the current value—to make it affordable for a typical young person to manage an 80 per cent mortgage at current interest rates.

Alternatively, the study finds, typical full-time earnings would need to increase to $100,600/year—nearly double current levels. Based on the last decade, actual earnings are expected to be flat.

READ MORE: Public forum fails to ease Rutland residents’ frustration over McCurdy house

READ MORE: Kelowna ranked 7th most expensive rental market in Canada

The study also states it would take typical Kelowna residents between 25 and 34-years-old, 13 years to save up enough for a 20 per cent down payment on an average home – nine more years than when today’s ageing population started as young people.

Kelowna’s 13 years was equal to the nationwide average in this stat but is among and above cities with larger populations including Montreal at 11 years, Ottawa and Calgary at 10 years and Edmonton and Halifax at nine years.

Metro Vancouver and Toronto ranked the highest, taking 29 and 21 years respectively.

The study’s definition of affordable was taken from the Canada Mortgage and Housing Corporation (CMHC), as not spending more than 30 per cent of pre-tax earnings on housing.

@michaelrdrguez

michael.rodriguez@kelownacapnews.com

Like us on Facebook and follow us on Twitter.